If you’ve already received a cash advance but your legal battle is dragging on, you might be wondering why some lenders say “yes” to more money while others say “no.” It usually isn’t about your credit score or your job—it’s about the math of your case.

At Baker Street Funding, we believe that understanding case equity is the best way to protect your final settlement. Whether you are looking for a “second look” from your current lender or considering a buyout to lower your rates, the amount you can receive depends on how much “room” is left in your lawsuit.

Below, we break down the exact equation underwriters use to determine if you qualify for additional funding and how you can preserve your case value for the long haul.

Need to apply now?

Current Baker Street Clients: Visit our Additional Funding page or contact your funding expert directly request a supplemental advance.

New Clients with a Loan Elsewhere: See our Buyouts & Refinancing guide to see if you can switch and save.

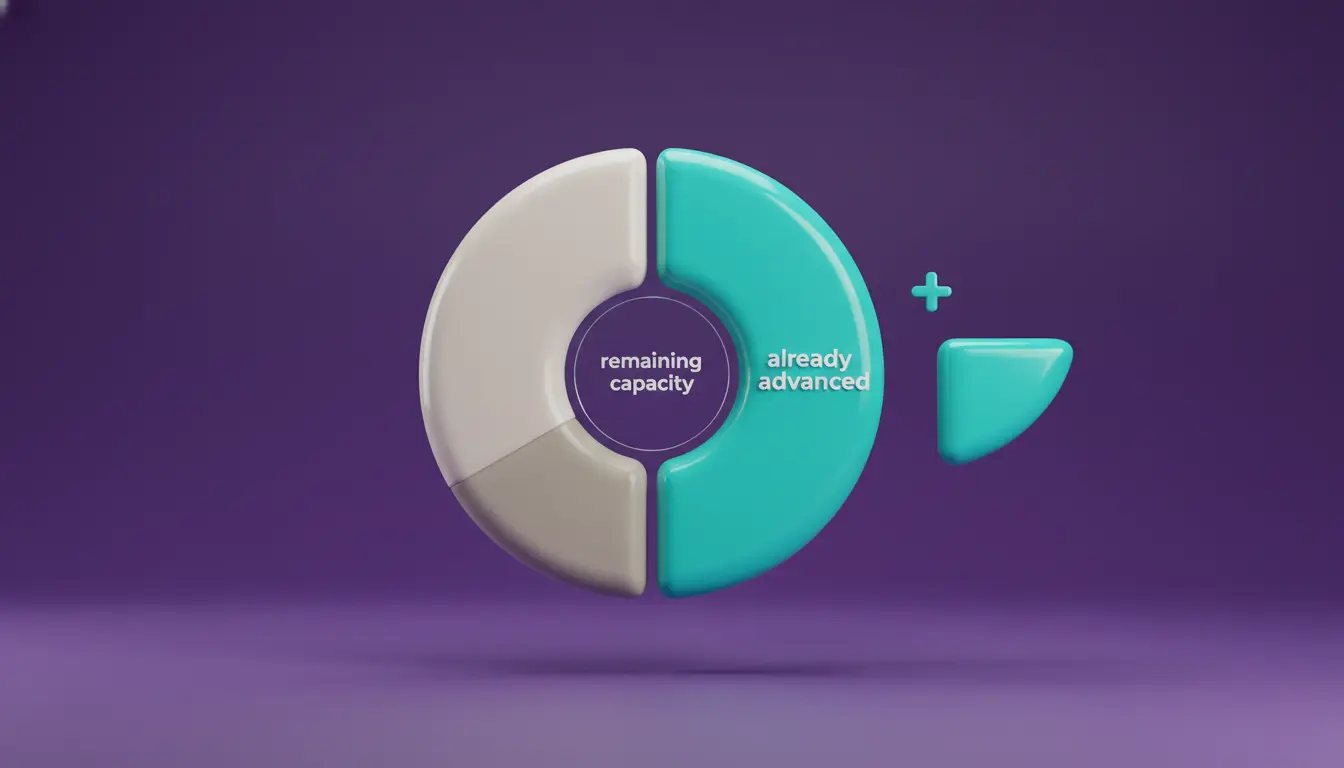

What is “Case Equity” in Legal Funding?

Most plaintiffs think of their case in terms of the final settlement check. However, underwriters look at Case Equity—the amount of money likely to be left over after all “prior liens” are paid.

Here is the step-by-step math used to find that number:

Step 1: The Conservative Case Value

Legal funding underwriters don’t use the “best-case scenario” number. They look at a conservative estimate of what your case would settle for today based on similar verdicts in your state.

Example: Your attorney expects a $100,000 settlement.

Step 2: Deduct Mandatory Liens & Fees

Before you see a dime, certain “priority” debts must be paid from the settlement. Underwriters subtract these first:

- Attorney Fees: Usually 33% to 40% (e.g., $33,000).

- Legal Costs: Filing fees, expert witnesses, etc. (e.g., $2,000).

- Medical Liens: Unpaid hospital bills or “Letters of Protection” (e.g., $15,000).

- Total Mandatory Deductions: $50,000.

Step 3: Calculate the “Lien Load” (Existing Loans)

Next, they look at what you already owe to funding companies. This is where the interest structure matters.

Current Loan Payoff: If you borrowed $10,000 and it has grown to $15,000 due to interest, that $15k is your current lien load.

Step 4: Finding the Net Equity

Now, the math reveals how much “real” value is left:

$100,000 (Value) – $50,000 (Fees/Medical) – $15,000 (Existing Loan) = $35,000 Net Equity

Step 5: The 10% Safety Cap

Most ethical lenders will not allow the total amount borrowed to exceed 10% of the Conservative Case Value (Step 1).

In this example ($100k case), a 15% cap means you can borrow a total of $15,000.

Since you already have a $15,000 payoff, a legal funding company might determine you have “maxed out” your equity until the case value increases (e.g., through a new surgery or a successful deposition).

Why the “10% to 20% Rule” Exists

Reputable lenders rarely fund more than 10% of a case’s conservative value. Here’s why:

- Protecting the Plaintiff: If you borrow 50% of your case value, interest and fees could leave you with $0 at the end of the trial.

- Attorney Cooperation: Lawyers are less likely to sign off on non-recourse funding if they feel the “lien load” is too heavy, as it makes the case harder to settle.

How Existing “Payoffs” Affect New Funding

When you apply for additional funding, the “payoff” (the principal plus all accrued interest) of your current loan is the most important number.

If your current funder uses compounding interest, your “payoff” grows every month, eating into the remaining value of your case and shrinking the “room” you have to qualify for more funding later. But with simple interest and a cap—like the terms offered by Baker Street Funding—your payoff grows much slower, preserving more of your case equity.

This means you’re more likely to qualify for a “second look” or additional funding six months or a year down the line, without worrying about runaway interest rates.

Having trouble getting a payoff letter from your current lender for a buyout? Here’s what you can do.

Protecting Your Settlement: The Baker Street Advantage

Pro Tip: Preserve Your Equity with Simple Interest

The biggest threat to your case equity isn’t time—it’s compounding interest. Many funding companies charge interest on the interest, meaning your “lien load” grows exponentially every month.

At Baker Street Funding, we use a 2.95% to 3.4% simple interest structure (non-compounding) on most cases. This means your payoff is only calculated on the original amount you borrowed.

Keeping your payoff growth linear and predictable, means more “net equity” stays in your settlement, giving you more financial breathing room if your case takes longer than expected.

Why Injured Plaintiffs Trust Baker Street Funding

We don’t just provide checks; we provide a bridge to justice. When you partner with us, you aren’t just a case number—you get:

- A Dedicated Funding Associate: You’ll work with one expert who understands the delicate nature of your personal injury claim.

- The 10% Safety Rule: We won’t over-leverage your pre-settlement case. We help you borrow responsibly to protect your final recovery.

- Non-Recourse Protection: If you don’t win your case, you owe us absolutely nothing.

Ready to Secure the Value of Your Case?

Whether you need a “second look” at your current Baker Street case or you’re looking to escape a high-interest loan with another funding company, our team is ready to help.

Current Clients: Contact us at (888) 7113599 to request more funds.

New to Us? Apply for a Buyout & Lower Your Rates.