You apply for funds

Send us the basic details about your case, your attorney, and current funding. No credit checks.

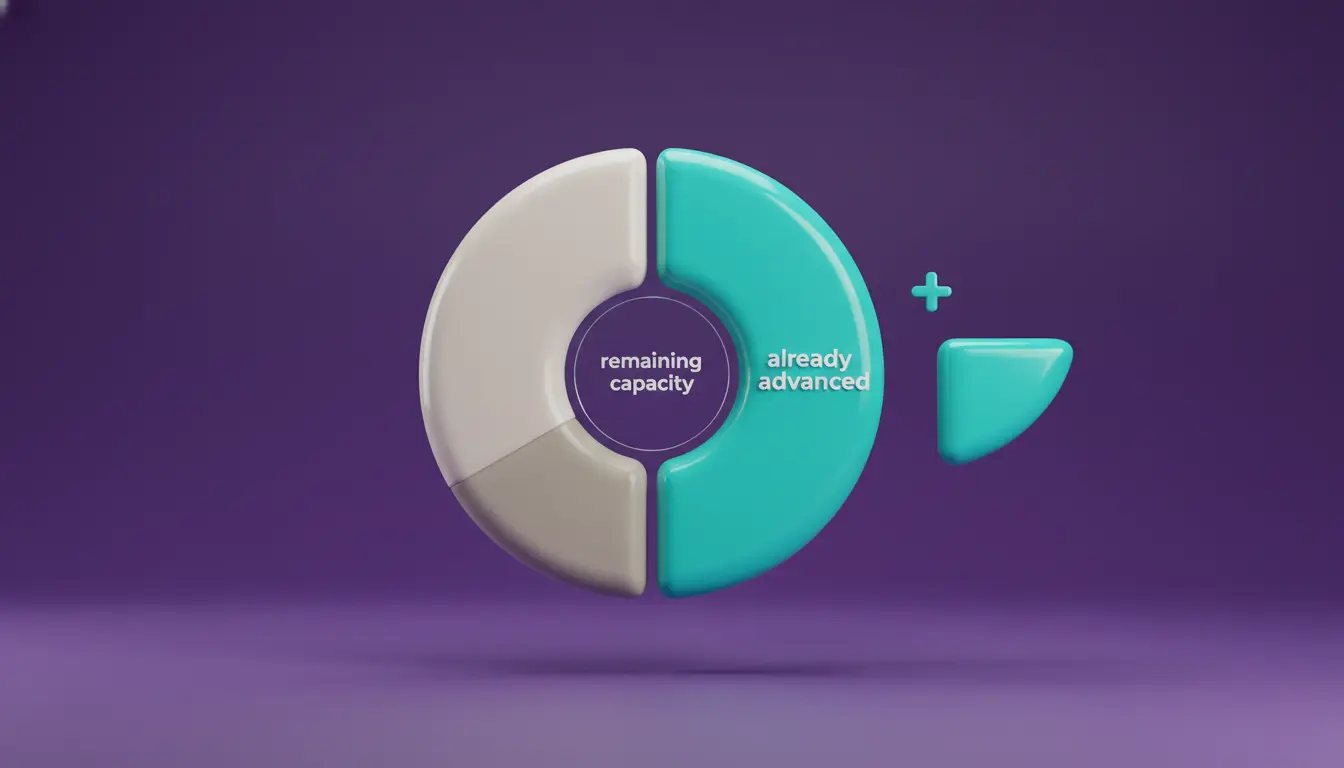

We request a payoff letter

It shows exactly what you owe on the current agreement right now, and if there is remaining “equity” to cover both the old debt and the new advance.

We review your case with your lawyer

We look at the case value, current posture, existing payoff, and whether enough room remains in the claim.

Legal funding decision

If the numbers make sense, you and your attorney receive a new Baker Street Funding agreement.

![]()

Review and sign the agreement

You and your attorney review and sign the paperwork before funds are disbursed.

Pay off and new funding

Upon contract execution, we pay your original pre-settlement loan in full. You receive the remaining balance of the new, larger advance.